In a market full of noise, Return on Equity (ROE) cuts through and answers one simple question: How efficiently is a company using your money?

This cement sector screener highlights companies generating 15%+ ROE, and that’s where things get interesting.

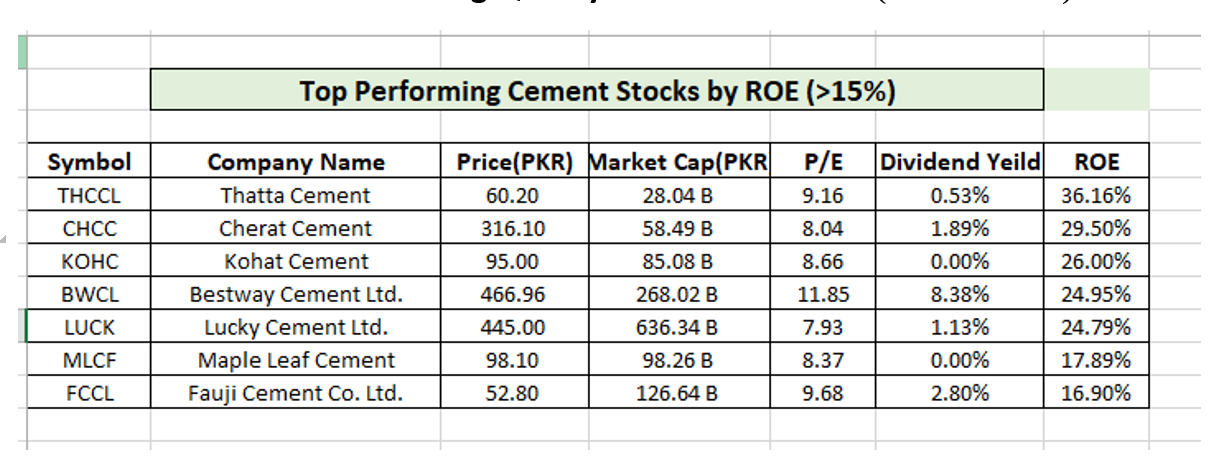

At the top, Thatta Cement (THCCL) stands out with a striking 36% ROE. That’s not just performance it signals pricing power, cost control, or both. Similarly, Cherat Cement (CHCC) and Kohat Cement (KOHC) operating in the 25–30% range suggest strong business models that can sustain profitability even in cyclical conditions.

But here’s where investors need to go deeper.

High ROE alone isn’t enough. You need to ask:

- Is this ROE sustainable or cyclical?

- Is it driven by efficient operations or high leverage?

- Are earnings being distributed (dividends) or reinvested for growth?

For instance, Bestway Cement Ltd (BWCL) and Fauji Cement (FCCL) combine solid ROE with strong dividend yields, making them attractive for income-focused investors. On the other hand, companies with low or zero dividends may be reinvesting a positive sign if returns remain high.

Also notice the reasonable P/E ratios across the board. This suggests the sector isn’t overheated, despite strong profitability.

Investor takeaway:

Don’t just chase high ROE. Combine it with valuation, dividend policy, and sustainability. That’s how you separate temporary performers from long-term compounders in the cement sector.

Disclaimer: This report is provided solely for information purpose only and we have tried to ensure the correctness of the figures but there may still be discrepancies, for further verification of data please do visit official websites. The company accepts no responsibility what so ever for any direct or indirect consequential loss arising from use of this report.