Monday could prove decisive for the KSE-100. The index has already lost its short- and medium-term trend structure on the daily chart and now sits just above the 50-week exponential moving average (152,287.73), the final technical support on the weekly timeframe. With geopolitical tensions driving oil prices higher and the State Bank of Pakistan (SBP) due to announce its policy decision the same day, the market enters the new week facing a convergence of technical and macro risks.

Daily View

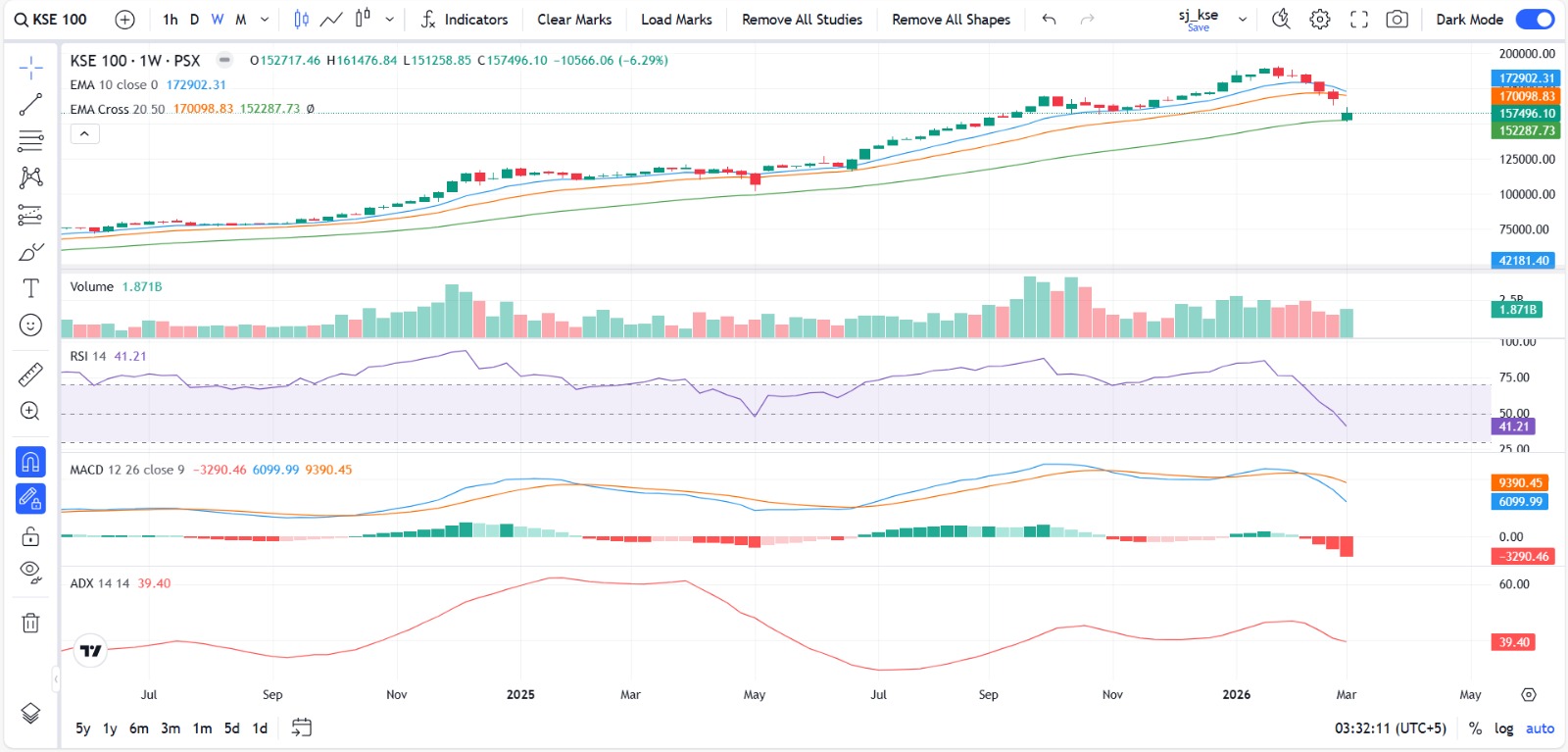

From a purely technical standpoint, the daily chart already signals that the correction has moved beyond a routine pullback.

The index is trading below the 10-day (162,297.18), 20-day (167,816.61) and 50-day (172,768.92) exponential moving averages, a cluster that normally defines the prevailing short-term trend. Once price slips below this structure, the technical regime typically shifts into distribution, where rebounds tend to be corrective rather than the beginning of a sustained advance.

Momentum indicators reinforce this view. The RSI has slipped into the mid-30s, reflecting persistent downside pressure and weak buying interest. While readings in this zone can occasionally precede tactical rebounds, they more commonly signal that sellers still dominate the market.

The MACD structure remains clearly bearish. The MACD line sits well below the signal line and the histogram continues to print negative values, confirming that downside momentum remains firmly in control. Until this relationship begins to stabilise, rallies are likely to remain temporary relief moves rather than durable reversals.

Trend strength provides additional confirmation. The ADX has climbed into the mid-40s, indicating that the current directional move has developed real intensity. Because ADX measures trend strength rather than direction, its elevated level simply confirms that the prevailing move, in this case downward, is not merely noise but a genuine trend.

In practical terms, the daily chart no longer offers meaningful structural support.

Weekly View

That shifts attention to the weekly timeframe, which now carries far greater significance.

The KSE-100 is currently holding just above its 50-week exponential moving average (152,287.73). Historically, this level has served as an important institutional support during corrections within longer bull markets. When markets retreat to this moving average, the outcome often determines whether the broader uptrend survives or transitions into a deeper correction.

However, the medium-term structure has already weakened. The index has slipped below the weekly 10-week (172,902.31) and 20-week (170,098.83) EMAs, signalling that upward momentum has deteriorated materially. Momentum indicators echo this warning.

Weekly RSI has declined toward the low-40s, showing that trend strength has faded but has not yet reached levels typically associated with a durable bottom. The weekly MACD has also rolled over into negative territory, a development that usually carries greater weight than similar shifts on the daily chart because weekly momentum changes tend to persist longer.

Trend strength remains elevated on this timeframe as well, with weekly ADX near the high-30s. This suggests that the directional move underway still has energy.

Verdict

The implication is straightforward. The weekly 50-EMA (152,287.73) now represents the market’s last major technical support. A sustained break below it would likely signal the beginning of a broader downtrend rather than a simple correction.

The macro backdrop increases the stakes.

The escalating Iran-Israel-US confrontation has already begun to push global oil prices higher. For Pakistan, which remains heavily dependent on imported energy, rising crude prices quickly translate into higher domestic fuel costs and renewed inflation pressure.

Petrol prices in Pakistan have already begun to rise in response to global markets. If oil continues to climb, the inflation outlook becomes more complicated just as SBP prepares to announce its next policy decision.

Industry has been hoping for a rate cut, but rising inflation expectations and the energy shock created by the conflict could constrain the central bank’s room to ease aggressively.

All of these elements converge on Monday.

Financial history contains enough examples of severe Monday selloffs to remind investors that weekends often allow geopolitical developments and policy uncertainties to accumulate before markets reopen; the fabled Black Monday syndrome. While such comparisons should never be made casually, the current setup leaves little margin for complacency.

Technically, the market is already fragile. If the weekly 50-EMA holds, oversold conditions could trigger a relief rally. But if that support fails decisively, the KSE-100 would likely enter a deeper bearish phase where rallies are sold rather than sustained.

In that sense, Monday is not merely the start of another trading week. It is the moment when the market must decide whether its long-term trend remains intact or begins to break down.

.png "The Relief Rally: Why the PSX Welcomed Budget FY27")