Pakistan’s pioneering all-steel radial tyre manufacturer files prospectus to raise up to Rs. 7.8 billion — one of the largest industrial IPOs on the PSX in recent years.

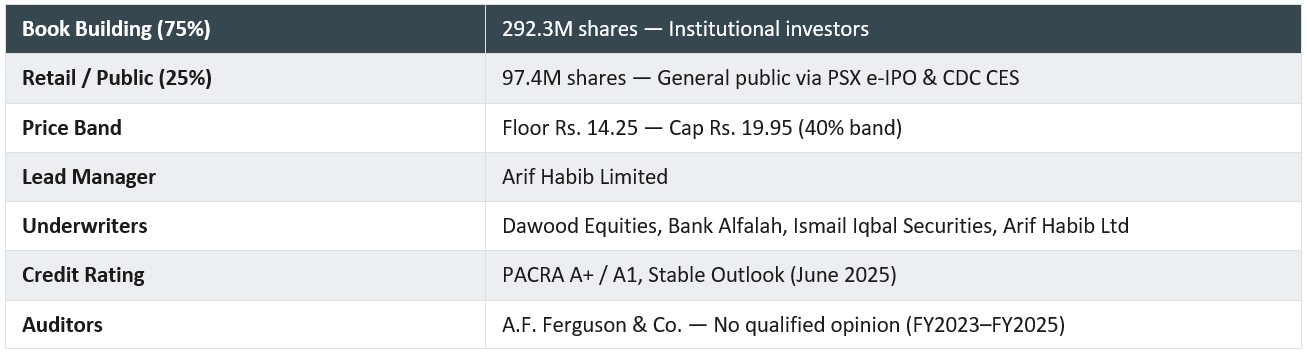

Service Long March Tyres Limited (SLM) has officially filed its Draft Prospectus with the Pakistan Stock Exchange and SECP for an initial public offering. The company is offering approximately 389.7 million ordinary shares at a floor price of Rs. 14.25 per share (with a 40% price band capping at Rs. 19.95), targeting gross proceeds of Rs. 5.6–7.8 billion.[1] Here’s everything you need to know.

Who Is SLM?

Born out of a 2019 joint venture between the Servis Group and China’s Chaoyang Long March Tyre Co. Ltd., SLM went from incorporation to commercial production in just over two years. Today, it operates a 50-acre facility in Nooriabad, Sindh — Pakistan’s first Sole Enterprise Special Economic Zone — and holds Greenfield Industrial Undertaking status from the FBR, granting tax concessions until June 2032.[2]

The company’s TBR tyres carry certifications that read like an international passport: DOT (USA), E-Mark (Europe), GSO (GCC), INMETRO (Brazil), NRCS (South Africa), and ISO 9001:2015. And the market has noticed — SLM commands an estimated 55% share of Pakistan’s domestic all-steel tyre segment.[3]

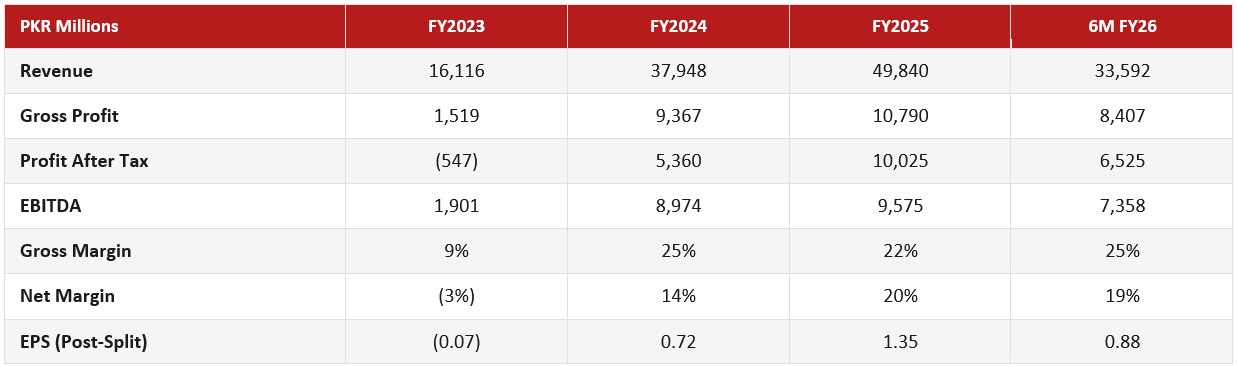

Exports tell an equally compelling story. Revenue from international markets jumped from Rs. 5.07 billion in FY2023 to Rs. 15.25 billion in FY2025, with the first half of FY2026 already clocking Rs. 9.87 billion. The USA and Brazil are the biggest buyers, and the company is targeting $100 million in annual exports by FY2027.[4]

How the IPO Is Structured

Arif Habib Limited is leading the deal as Consultant to the Issue. The retail portion is fully underwritten by four firms.[5]

Where the Money Goes

The Big Bet: SLM is building a Passenger Car Radial (PCR) tyre factory at Nooriabad. Total project cost: Rs. 22.56 billion. Funding: 50% long-term loan, 25% internal cash, 25% IPO proceeds.[6] Commercial production is targeted for January 2028, starting at 2.0 million tyres/year, scaling to 2.5 million (FY2029) and 3.0 million (FY2030).[7] |

The Numbers That Matter

SLM went from a net loss in FY2023 to Rs. 10 billion in profit in just two years. Revenue has grown at a CAGR of 75.86% since operations began. The first half of FY2026 is already tracking ahead.[8]

The company also runs 12 MW of solar power and is adding a 7.5 MW wind turbine — cutting costs and carbon in one move.[9]

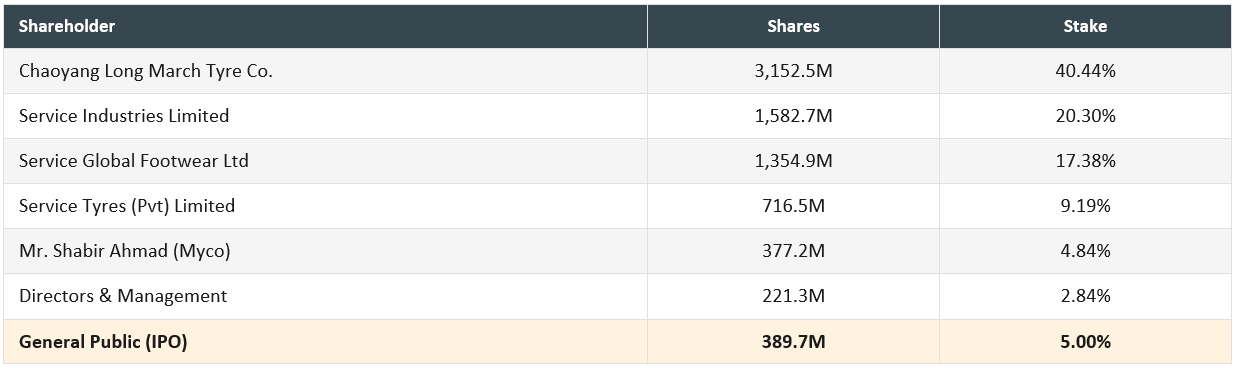

Who Owns What (Post-IPO)

Source: SLM Draft Prospectus, Section 3.2[10]

Why This Market, Why Now

Pakistan’s tyre market is forecast to reach $2.71 billion by 2030, yet the country imports the vast majority of what it consumes. The passenger car segment — exactly where IPO proceeds are headed — is growing fastest, and the aftermarket (nearly 75% of all demand) ensures a recurring revenue base that doesn’t depend on new car sales alone.[11] With virtually no domestic PCR manufacturing to speak of and China dominating the supply pipeline, SLM isn’t just entering a market — it’s creating a category.[12]

What Happens Next

The Draft Prospectus is on the PSX website for public comment until April 21, 2026. Once finalised, book-building and retail subscription dates will be announced. Investors can access full details at psx.com.pk, slmtires.com, or arifhabibltd.com. Applications will be accepted through PSX’s e-IPO platform and CDC’s Centralized E-IPO system.[13]

| DISCLAIMER: This blog post is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities. The information has been compiled from publicly available sources including the SLM Draft Prospectus filed with the PSX and SECP, company annual reports, and media reports. Forward-looking statements involve risks and uncertainties, and actual results may differ materially. Investment in IPOs carries significant risk, including the potential loss of capital. Prospective investors should conduct their own due diligence and consult qualified financial, legal, and tax advisors before making any investment decisions. This post has not been approved by the SECP. Securities may not be offered or sold without delivery of a prospectus meeting the requirements of applicable securities laws. |

[1]SLM Draft Prospectus, PSX Notice PSX/N-416, April 14, 2026; Section 2.

[2]SLM Draft Prospectus, Section 2.1. SEZ status, Greenfield Industrial Undertaking, tax concessions until June 30, 2032.

[3]SLM Draft Prospectus, Section 2.1. Certifications and 55% market share (management estimate, footnote 2).

[4]SLM Draft Prospectus, Section 2.1 – Export Revenue table. Target figures from Business Recorder, April 10, 2026.

[5]SLM Draft Prospectus, Cover page and Section 2.4. Underwriters in Supplement to Prospectus.

[6]SLM Draft Prospectus, Sections 2.5 and 2.5.1 – Purpose of Issue and Source of Funding.

[7]SLM Draft Prospectus, Section 2.1. PCR capacity ramp-up and January 2028 commencement.

[8]SLM Draft Prospectus, Section 2.8. Audited by A.F. Ferguson & Co. (FY23–25); 6M FY26 unaudited.

[9]SLM Draft Prospectus, Section 2.1. PACRA rating June 27, 2025. Solar/wind capacity.

[10]SLM Draft Prospectus, Section 3.2 – Pattern of Shareholding.

[11]Mordor Intelligence; IMARC Group; IndexBox – Pakistan Tyre Market reports.

[12]Mordor Intelligence – PCR CAGR 7.38%, aftermarket 74.91%. Research and Markets 2026–2034.

[13]SLM Draft Prospectus, Cover page. E-IPO platforms and download links.